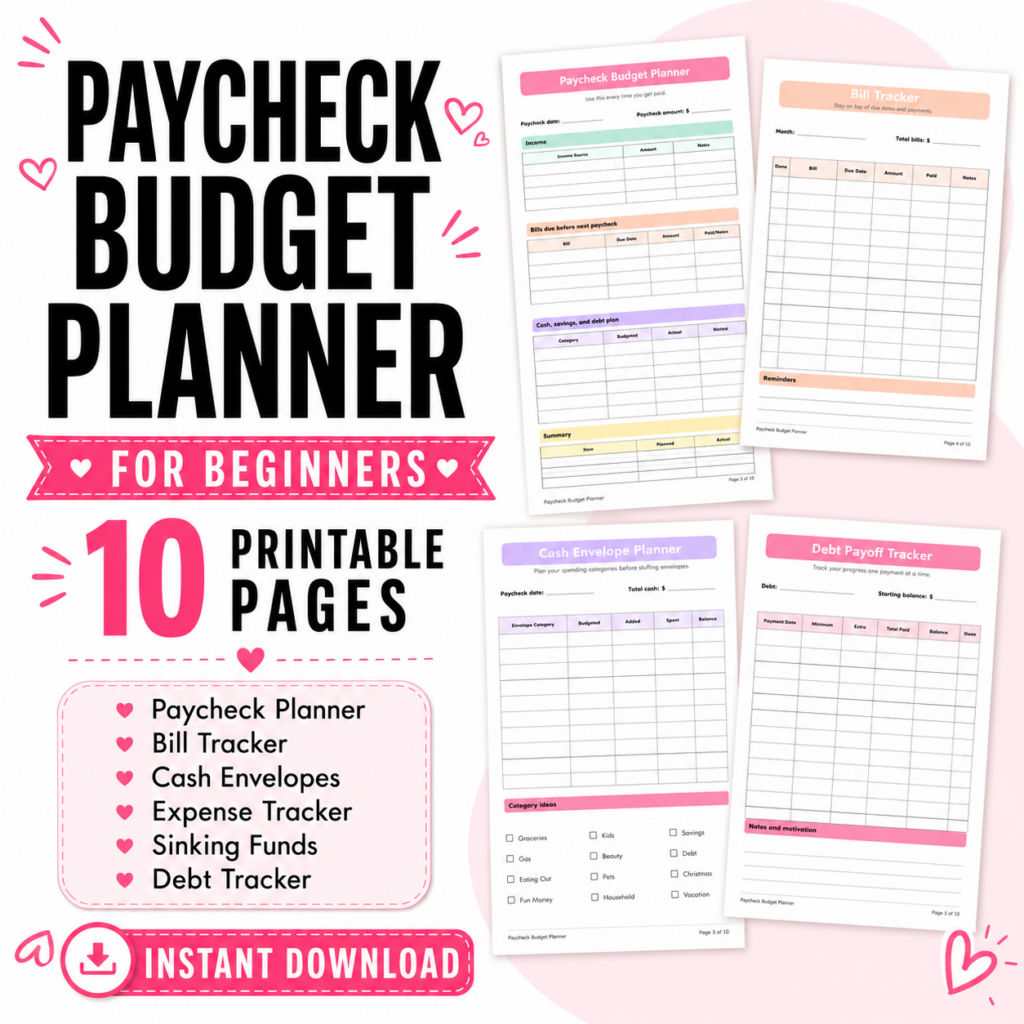

How to Use a Paycheck Budget Planner for Beginners

If you ever feel like your paycheck disappears way too fast, you are definitely not alone.

One minute the money hits your account, and the next minute you are wondering where it all went. Bills, groceries, gas, subscriptions, random Target runs, coffee, kids, emergencies, and little purchases can add up so quickly.

That is exactly why a paycheck budget planner can be so helpful.

Instead of trying to budget for the whole month all at once, a paycheck budget planner helps you make a simple plan for each paycheck before you spend it.

This is especially helpful if you are paid weekly, biweekly, twice a month, or if your income changes from paycheck to paycheck.

In this beginner-friendly guide, I will show you how to use a paycheck budget planner step by step so you can feel more organized, less stressed, and more in control of your money.

What Is a Paycheck Budget Planner?

A paycheck budget planner is a simple budgeting tool that helps you decide where your money will go every time you get paid.

Instead of looking at your budget as one big monthly plan, you break it down by paycheck.

For example, if you get paid every two weeks, you would create a separate budget for each paycheck.

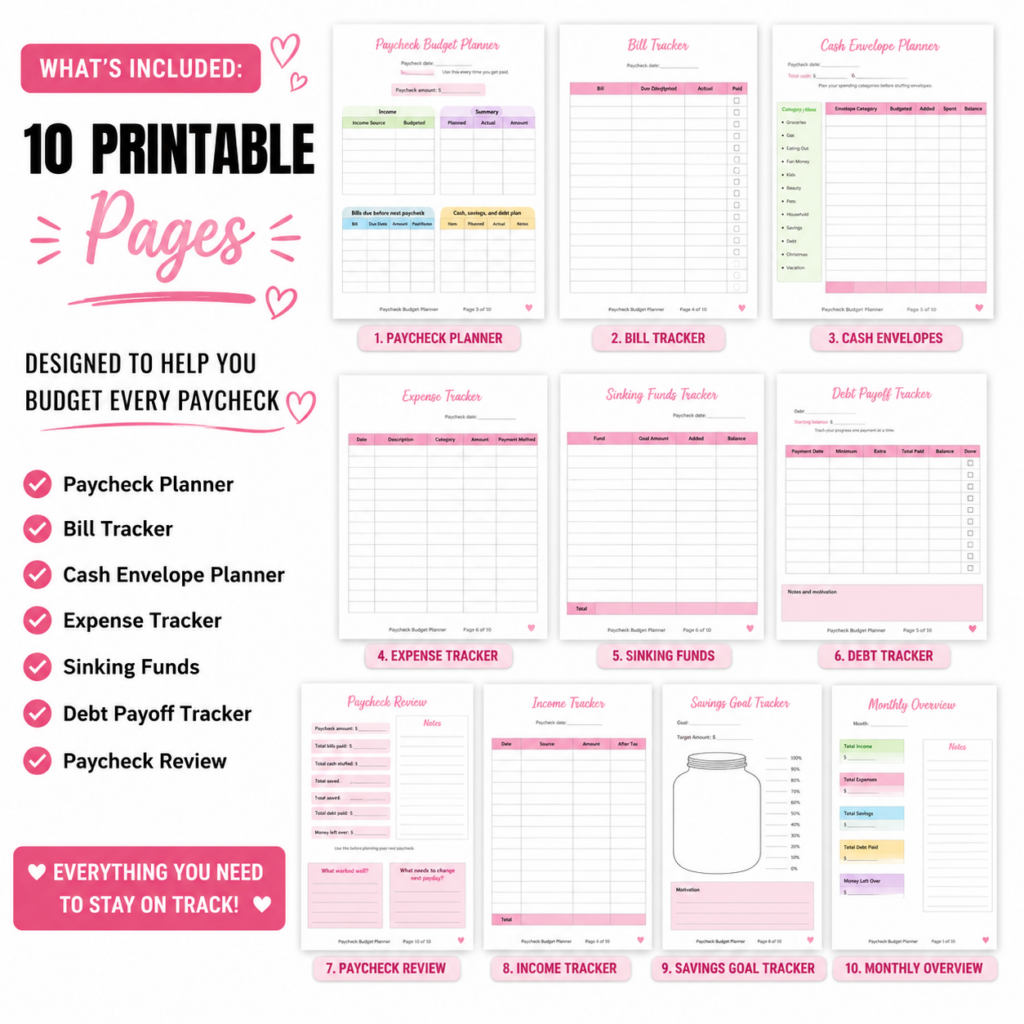

Your paycheck budget planner usually includes:

- Your paycheck amount

- Bills due before your next paycheck

- Variable expenses like groceries and gas

- Savings goals

- Debt payments

- Cash stuffing categories

- Leftover money

The goal is simple: give every dollar a job before you spend it.

Why Budgeting by Paycheck Works So Well

Budgeting by paycheck feels easier because it is more realistic.

A monthly budget can look good on paper, but sometimes the timing does not work. You may have enough income for the whole month, but if several bills are due before your next paycheck, you can still feel broke or stressed.

That is why paycheck budgeting works so well.

It helps you answer important questions like:

- What bills do I need to pay with this paycheck?

- How much money do I need for groceries until I get paid again?

- Can I put money into savings this time?

- How much cash should I stuff into each envelope?

- Do I have enough for extra spending?

This makes your money feel more organized and helps you avoid overspending right after payday.

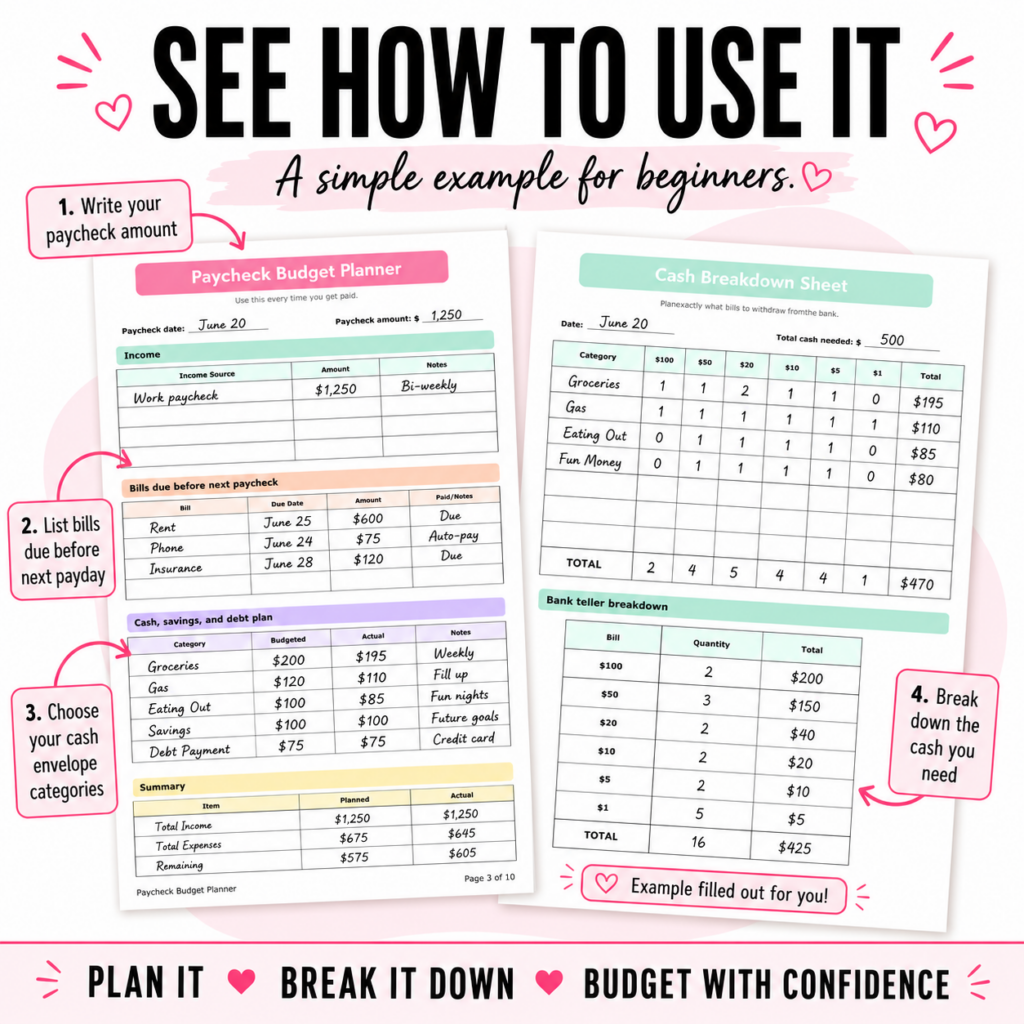

Step 1: Write Down Your Paycheck Amount

The first step is to write down how much money you actually have to work with.

Use your take-home pay, not your gross pay.

Your take-home pay is the amount that actually hits your bank account after taxes, insurance, retirement, and other deductions.

For example:

Paycheck amount: $1,250

This is the number you will use to create your paycheck budget.

If your income changes, use your lowest realistic estimate. It is always better to budget with a smaller number and have extra money left over than to budget too high and come up short.

Step 2: List the Bills Due Before Your Next Paycheck

Next, look at your calendar and write down every bill that is due before your next payday.

This can include:

- Rent or mortgage

- Car payment

- Insurance

- Phone bill

- Internet

- Credit cards

- Loan payments

- Utilities

- Subscriptions

- Childcare

- Any automatic payments

This step is important because the timing of your bills matters.

For example, if you get paid on the 1st and your next paycheck comes on the 15th, you only need to include the bills due between the 1st and the 14th.

You do not need to pay every bill with one paycheck unless it is actually due before the next one.

This is what makes a paycheck budget planner so useful.

Step 3: Plan Your Everyday Spending

After bills, plan for the things you need to buy before your next paycheck.

These are usually called variable expenses because the amount can change.

Common everyday spending categories include:

- Groceries

- Gas

- Household items

- Eating out

- Kids’ expenses

- Beauty or personal care

- Pet supplies

- Medicine

- School expenses

- Miscellaneous spending

Be honest with yourself here.

If you usually spend $250 on groceries between paychecks, do not write $100 just because it looks better. A budget only works when it matches your real life.

You can always lower spending over time, but your first goal is to create a budget that is realistic.

Step 4: Add Your Savings Goals

Once you have your bills and everyday expenses listed, decide how much you want to save from this paycheck.

Your savings categories may include:

- Emergency fund

- Car maintenance

- Christmas

- Birthdays

- Vacation

- Back to school

- Medical expenses

- Home savings

- Beauty fund

- Personal spending

- Sinking funds

This is where paycheck budgeting works beautifully with cash stuffing.

Instead of waiting to see what is left over at the end, you plan your savings first.

Even if you can only save $5, $10, or $20 per paycheck, it still counts. Small amounts add up when you are consistent.

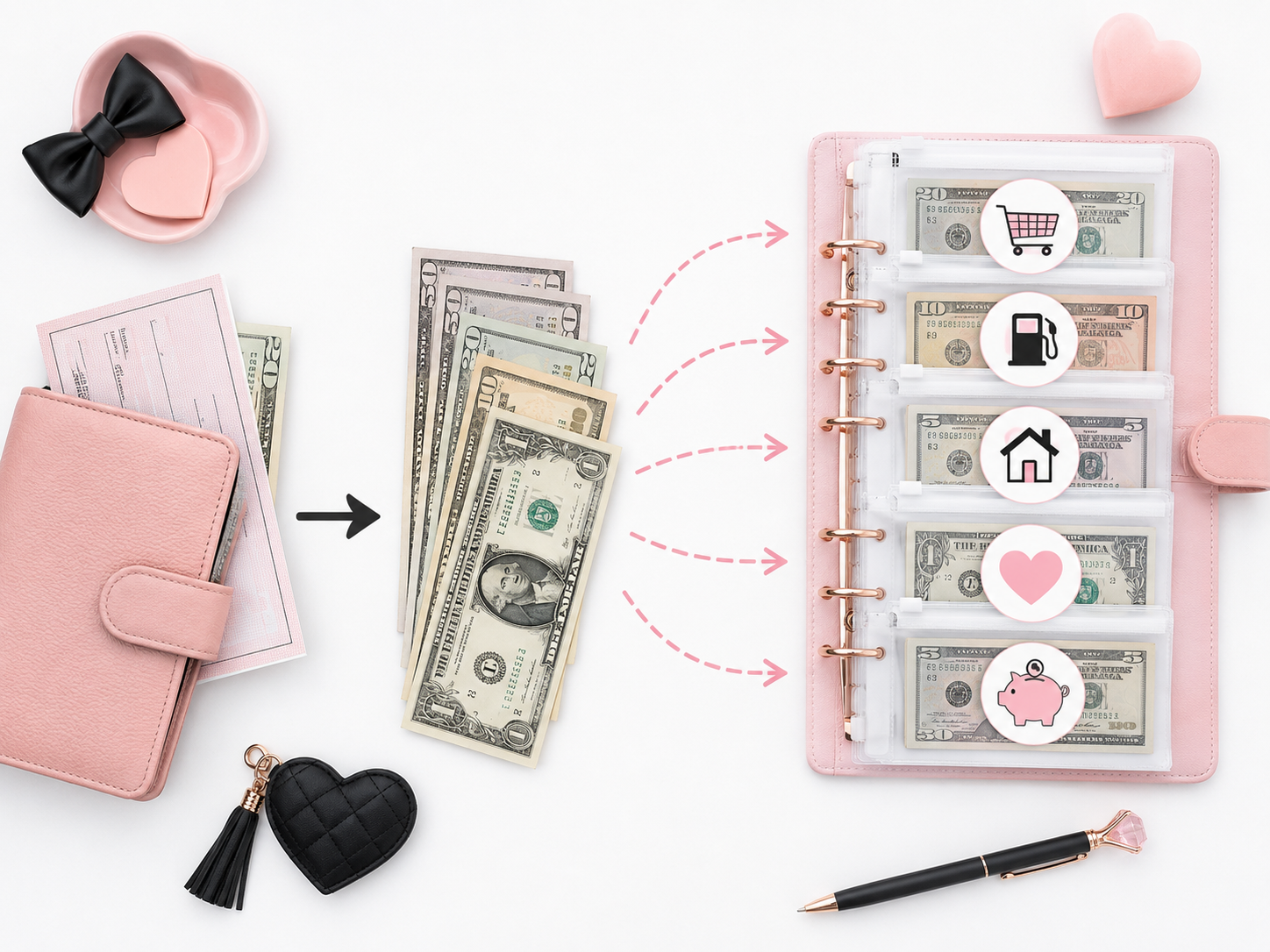

Step 5: Choose Your Cash Stuffing Categories

If you use the cash envelope system, your paycheck budget planner will help you decide how much cash to stuff into each category.

For example, you may have envelopes for:

- Groceries

- Gas

- Eating out

- Beauty

- Fun money

- Kids

- Household

- Savings challenges

- Sinking funds

After you write your budget, you can withdraw the cash you need and divide it into your envelopes.

Example:

Groceries: $200

Gas: $80

Eating out: $40

Beauty: $25

Kids: $30

Savings challenge: $20

Total cash to withdraw: $395

This makes cash stuffing feel less random because your envelopes are based on your actual paycheck budget.

Step 6: Subtract Everything From Your Paycheck

Now it is time to do the math.

Start with your paycheck amount, then subtract:

- Bills

- Everyday expenses

- Savings

- Debt payments

- Cash stuffing money

The formula is simple:

Paycheck amount – planned expenses = leftover money

For example:

Paycheck: $1,250

Bills: $600

Groceries and gas: $280

Savings: $100

Cash envelopes: $150

Debt payment: $75

Leftover: $45

That leftover money can stay in your bank account as a small buffer, go toward extra debt, or be added to savings.

Try not to leave too much money unplanned, because that is usually where overspending happens.

Step 7: Track Your Spending Until the Next Paycheck

A paycheck budget planner is not just for payday.

You also want to track your spending during the week or two before your next paycheck.

This helps you see if you are staying on budget or if you need to adjust.

You can track:

- How much you spent

- What category it came from

- How much money is left

- Any unexpected expenses

This step is especially helpful if you are new to budgeting because it shows you your real spending habits.

You may realize you spend more on food, beauty, coffee, Amazon, or little extras than you thought. That is not a reason to feel bad. It is just information you can use to improve your next budget.

Step 8: Review Before Your Next Payday

Before your next paycheck arrives, take a few minutes to review your budget.

Ask yourself:

- Did I have enough for bills?

- Did I overspend in any category?

- Did I forget any expenses?

- Did I save anything?

- What do I need to change next time?

This is where your budget starts getting better.

Your first paycheck budget may not be perfect, and that is completely normal. Budgeting is not about being perfect. It is about learning your money habits and making small improvements every payday.

Paycheck Budget Planner Example

-> Get your Paycheck Budget Planner here

Here is a simple example of how a paycheck budget could look:

Paycheck amount: $1,400

Bills due before next payday:

- Rent: $600

- Phone: $85

- Car insurance: $120

- Credit card: $50

Everyday spending:

- Groceries: $250

- Gas: $100

- Household: $40

- Eating out: $50

Savings and cash stuffing:

- Emergency fund: $50

- Christmas sinking fund: $25

- Beauty envelope: $20

- Savings challenge: $20

Leftover buffer: $10

This kind of plan helps you know exactly where your money is going before you spend it.

Common Paycheck Budgeting Mistakes

When you are first learning how to use a paycheck budget planner, there are a few common mistakes to watch for.

1. Forgetting small expenses

Small expenses can throw off your budget if you do not plan for them.

Things like school snacks, coffee, parking, beauty products, birthday gifts, and last-minute grocery runs should have a category.

2. Budgeting too tightly

Try not to budget every single dollar so tightly that you have no breathing room.

A small buffer can help you avoid stress if something costs more than expected.

3. Not checking bill due dates

Paycheck budgeting works best when you know exactly when your bills are due.

Always check the due dates before assigning bills to a paycheck.

4. Not being realistic

A budget should help you, not punish you.

If you know you need gas, groceries, or personal spending money, include it. A realistic budget is easier to stick to.

5. Giving up after one bad paycheck

Some paychecks will be harder than others.

Maybe you had an emergency, a birthday, a car repair, or a higher grocery bill. That does not mean budgeting is not working. It just means you adjust and keep going.

How a Paycheck Budget Planner Helps With Cash Stuffing

A paycheck budget planner and cash stuffing go perfectly together.

Your budget tells you how much money you have available.

Your cash envelopes help you physically separate that money into categories.

This makes it easier to avoid overspending because you can see exactly how much is left in each envelope.

For example, if your eating out envelope has $15 left, you know that is your limit until the next paycheck.

This is why so many beginners love using a paycheck budget planner before cash stuffing. It gives your cash stuffing routine more structure and purpose.

Final Thoughts

Learning how to use a paycheck budget planner can make budgeting feel so much easier.

Instead of wondering where your money went, you get to decide where it goes before you spend it.

Start simple. Write down your paycheck amount, list your bills, plan your everyday spending, add savings, and track what happens.

Your budget does not have to be perfect to be helpful.

The more you practice, the more confident you will feel with your money.

And if you are also using the cash envelope system, a paycheck budget planner is one of the best tools to help you decide exactly how much money to put into each envelope every payday.