Cash Stuffing for Beginners: How to Organize Your Paycheck

If you’ve ever looked at your bank account and wondered where your money went, cash stuffing might be a simple system worth trying.

Cash stuffing is a budgeting method where you divide your money into categories before you spend it. Instead of swiping your card for everything and checking your balance later, you decide ahead of time how much money goes toward groceries, gas, eating out, savings, debt, and other expenses.

It is simple, visual, and beginner-friendly.

The best part is that you do not need to be perfect with money to start. You just need a paycheck, a few categories, and a plan.

In this guide, I’ll show you how to start cash stuffing as a beginner, what categories to use, how to organize your paycheck, and how to use a cash breakdown sheet before going to the bank.

You can also use my Cash Stuffing Starter Kit for Beginners if you want a printable system with a paycheck budget planner, cash breakdown sheet, savings trackers, cash envelope templates, and more.

What Is Cash Stuffing?

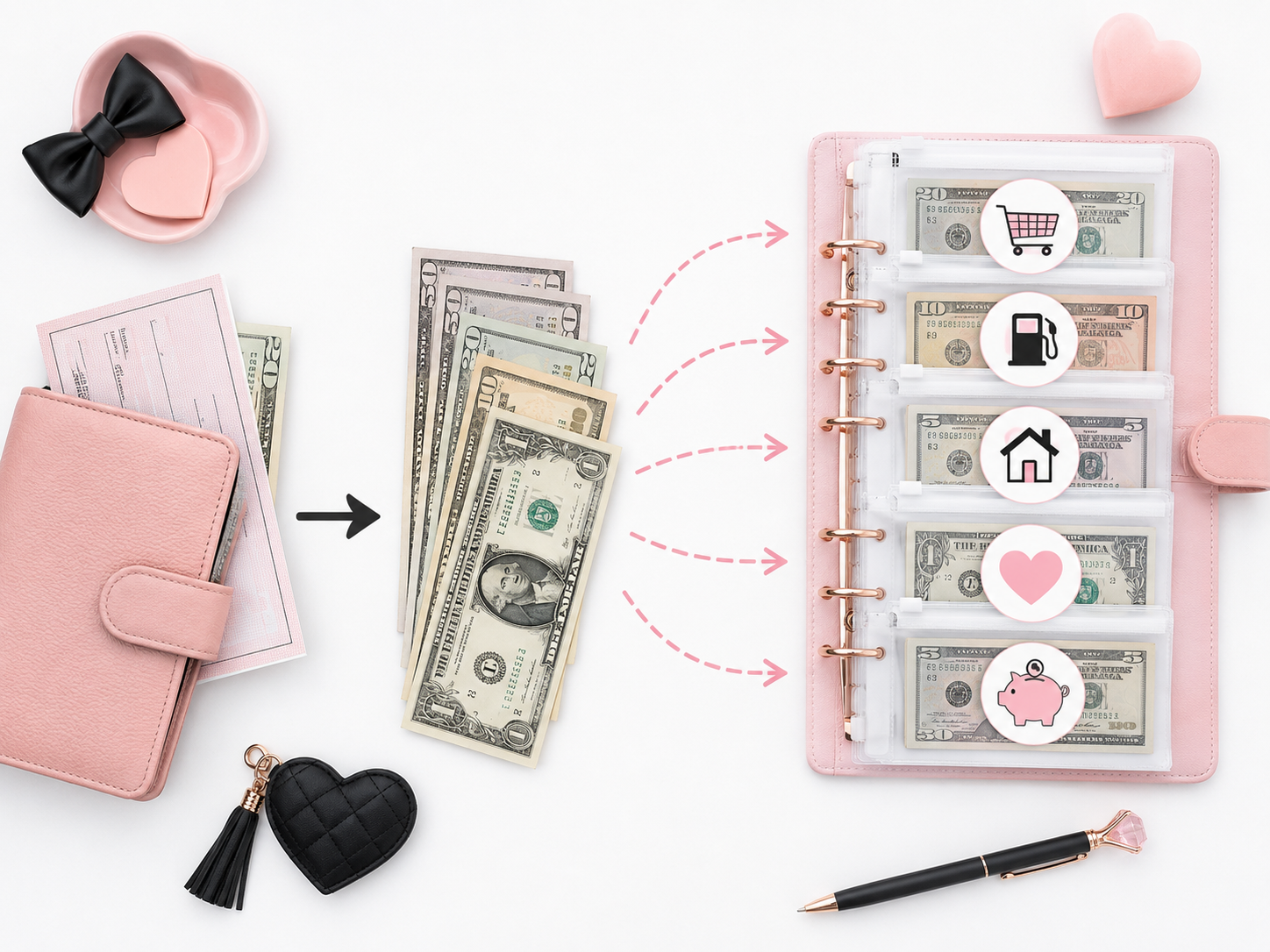

Cash stuffing is a budgeting system where you separate your money into different spending categories.

Traditionally, people use cash envelopes or a budget binder. Each envelope is labeled with a category, such as:

- Groceries

- Gas

- Eating out

- Fun money

- Beauty

- Kids

- Pets

- Emergency fund

- Savings

- Debt payoff

When you get paid, you decide how much money should go into each category. Then you place that amount of cash into the matching envelope.

For example, if your grocery budget is $200, you put $200 into your groceries envelope. Once that envelope is empty, you are done spending in that category until the next paycheck.

That is what makes cash stuffing so helpful. It gives your money a clear job before you spend it.

Why Cash Stuffing Works

Cash stuffing works because it makes your budget easier to see.

When all your money is sitting in one bank account, it can be hard to know what is already promised to bills, what is available to spend, and what should be saved.

With cash stuffing, you separate your money by purpose.

Instead of thinking, “I have $800 in my account,” you start thinking:

- $300 is for bills

- $200 is for groceries

- $80 is for gas

- $50 is for eating out

- $100 is for savings

- $70 is for debt

That small shift can make a big difference.

Cash stuffing can help you:

- Stop overspending in certain categories

- Stay ahead of bills

- Save for future expenses

- Build an emergency fund

- Pay down debt

- Be more intentional with each paycheck

It is also great for people who get paid weekly, biweekly, or irregularly because you can plan one paycheck at a time.

What You Need to Start Cash Stuffing

You do not need a complicated system to begin. Start simple.

Here are the basic things you need:

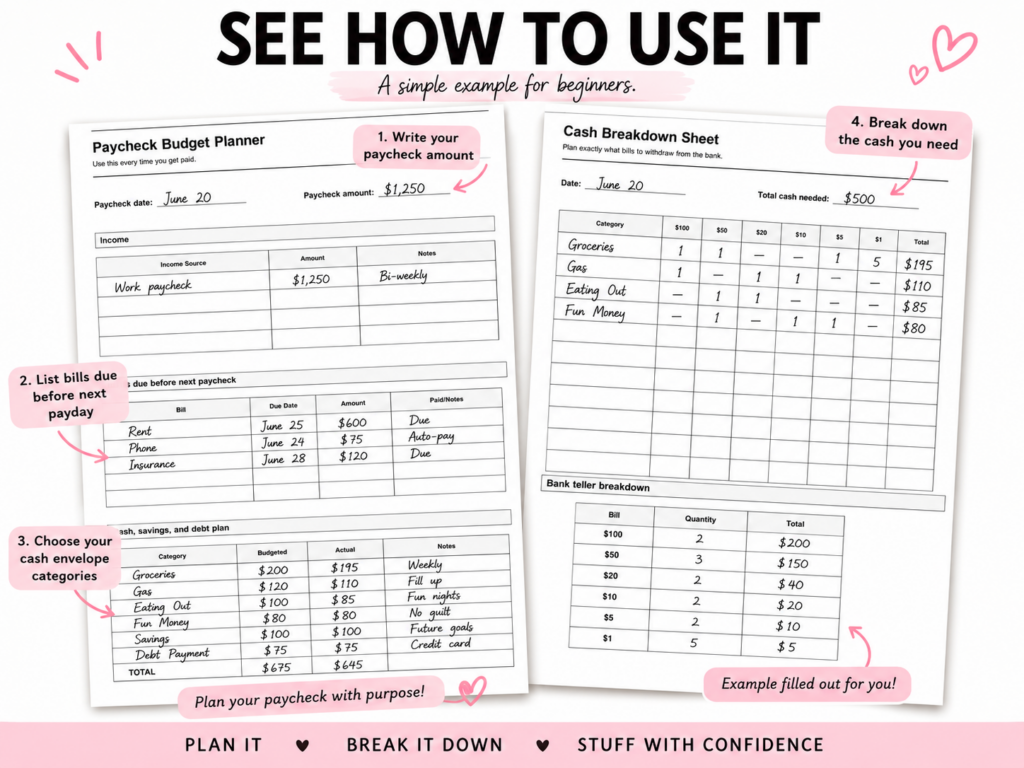

1. A Paycheck Budget Planner

A paycheck budget planner helps you organize one paycheck before you spend it.

You can write down:

- Paycheck date

- Paycheck amount

- Bills due before the next payday

- Cash envelope categories

- Savings goals

- Debt payments

- Leftover money

This is one of the most important pages because it helps you decide where your money needs to go first.

2. A Cash Breakdown Sheet

A cash breakdown sheet helps you figure out what bills to withdraw from the bank.

For example, if you need $200 for groceries, you may want:

- 1 hundred-dollar bill

- 2 fifty-dollar bills

Or you may want smaller bills if you plan to split the money into different envelopes.

A cash breakdown sheet keeps you organized so you do not have to guess at the bank.

3. Cash Envelopes

Cash envelopes are where you keep your money for each spending category.

You can use actual envelopes, printable envelopes, zipper pouches, or a small budget binder.

The important thing is that every category has a place.

4. Spending Trackers

Spending trackers help you write down what you spent and how much is left.

This is especially helpful when you are first starting because it shows you which categories are working and which ones need to be adjusted.

5. Sinking Fund Trackers

Sinking funds are savings categories for expenses that do not happen every paycheck but still need to be planned for.

Examples include:

- Christmas

- Birthdays

- Car repairs

- Back-to-school shopping

- Vacation

- Medical expenses

- Pet expenses

- Annual bills

Instead of being surprised by these expenses later, you save a little at a time.

Best Cash Stuffing Categories for Beginners

One mistake beginners make is starting with too many envelopes.

You do not need 20 categories on your first payday. Start with 3 to 8 categories and add more later.

Here are good beginner cash stuffing categories:

Everyday Spending Categories

- Groceries

- Gas

- Eating out

- Coffee

- Household items

- Fun money

- Beauty

- Clothing

Family Categories

- Kids

- School

- Baby items

- Pets

- Date night

- Family fun

Savings Categories

- Emergency fund

- Vacation

- Christmas

- Birthdays

- Car maintenance

- Medical

- Home repairs

Debt Categories

- Credit cards

- Personal loans

- Car loan

- Extra debt payment

The best categories are the ones where you tend to overspend or the expenses you want to prepare for ahead of time.

For many beginners, a good starting setup is:

- Groceries

- Gas

- Eating out

- Fun money

- Savings

- Debt

- Car maintenance

- Christmas

How to Start Cash Stuffing Step by Step

Here is a simple cash stuffing routine you can follow every payday.

Step 1: Write Down Your Paycheck Amount

Start with your total paycheck amount.

Example:

Paycheck amount: $1,250

This is the money you are working with until your next payday.

If you have extra income, such as tips, side hustle money, or cash gifts, write that down too.

Step 2: List Bills Due Before Your Next Paycheck

Before you stuff cash envelopes, look at the bills that are due before your next payday.

This may include:

- Rent or mortgage

- Utilities

- Phone bill

- Insurance

- Car payment

- Credit card payment

- Subscriptions

- Childcare

- Internet

Your bills should usually come first because those are already promised expenses.

Example:

- Rent: $600

- Phone: $75

- Insurance: $120

Total bills: $795

Now subtract your bills from your paycheck.

$1,250 – $795 = $455 left to budget

Step 3: Choose Your Cash Envelope Categories

Next, decide which categories you want to use cash for.

You do not have to use cash for every single expense. Many people keep bills digital and only use cash for variable spending.

Good cash categories include:

- Groceries

- Gas

- Eating out

- Fun money

- Beauty

- Household

- Kids

- Clothing

Example:

- Groceries: $200

- Gas: $100

- Eating out: $60

- Fun money: $40

Total cash envelopes: $400

Step 4: Add Savings or Debt Payments

After bills and cash categories, decide whether you can put money toward savings or debt.

This can be a small amount. Even $5, $10, or $20 is still progress.

Example:

- Emergency fund: $25

- Extra debt payment: $30

Total savings/debt: $55

Now your paycheck is fully planned:

- Bills: $795

- Cash envelopes: $400

- Savings/debt: $55

Total: $1,250

That means every dollar has a job.

Step 5: Fill Out Your Cash Breakdown Sheet

Now that you know how much cash you need, use a cash breakdown sheet to decide which bills to withdraw.

Example:

Groceries: $200

Gas: $100

Eating out: $60

Fun money: $40

Total cash needed: $400

Your bank teller breakdown might look like:

- $100 bills: 2

- $50 bills: 2

- $20 bills: 4

- $10 bills: 2

This makes it easier to stuff each envelope with the right amount.

Step 6: Stuff Your Envelopes

After withdrawing your cash, place the money into the correct envelopes.

Example:

Groceries envelope: $200

Gas envelope: $100

Eating out envelope: $60

Fun money envelope: $40

You can write the starting amount on each envelope or use a tracker to record the balance.

Step 7: Track Your Spending

As you spend from each envelope, write down what you spent.

For example:

Groceries envelope starting amount: $200

Grocery trip: -$85

Remaining balance: $115

Tracking helps you see where your money is going and keeps you from accidentally overspending.

Step 8: Review Before the Next Payday

Before your next paycheck, review what happened.

Ask yourself:

- Which envelopes worked well?

- Which categories ran out too fast?

- Did I forget any bills?

- Did I spend less than expected anywhere?

- What should I adjust next payday?

This step is important because your first cash stuffing setup will not be perfect. That is normal.

The goal is not perfection. The goal is learning your spending habits and improving each paycheck.

Cash Stuffing Example for One Paycheck

Here is a simple example of how someone might organize a $1,250 paycheck.

Paycheck

Paycheck amount: $1,250

Bills

Rent: $600

Phone: $75

Insurance: $120

Total bills: $795

Cash Envelopes

Groceries: $200

Gas: $100

Eating out: $60

Fun money: $40

Total cash envelopes: $400

Savings and Debt

Emergency fund: $25

Extra debt payment: $30

Total savings and debt: $55

Final Budget

Bills: $795

Cash envelopes: $400

Savings and debt: $55

Total planned: $1,250

This is a simple example, but it shows the main idea: every dollar is assigned before it disappears.

What Are Sinking Funds?

Sinking funds are one of the best parts of cash stuffing.

A sinking fund is money you save little by little for a future expense.

For example, Christmas happens every year. Car repairs happen eventually. Birthdays, school supplies, medical expenses, and vacations all cost money.

Instead of waiting until the expense shows up, you create a sinking fund and save a small amount each paycheck.

Examples:

Christmas fund: $25 per paycheck

Car maintenance fund: $20 per paycheck

Vacation fund: $30 per paycheck

Birthdays fund: $10 per paycheck

Sinking funds help you stay ahead and avoid relying on credit cards for predictable expenses.

Beginner Cash Stuffing Mistakes to Avoid

Cash stuffing is simple, but beginners often make a few common mistakes.

Starting With Too Many Envelopes

Do not try to create an envelope for everything right away. Start with your most important categories and build from there.

Forgetting Bills Due Before the Next Payday

Always check your bill due dates before stuffing cash. You do not want to spend money that was supposed to cover a bill.

Not Tracking Spending

If you only stuff envelopes but never track spending, it is harder to know what needs to change.

Making the Budget Too Strict

Your budget should help you, not make you feel trapped. Give yourself a realistic amount for categories like food, gas, and fun money.

Quitting After One Imperfect Week

Your first week may be messy. That does not mean the system failed. It just means you are learning.

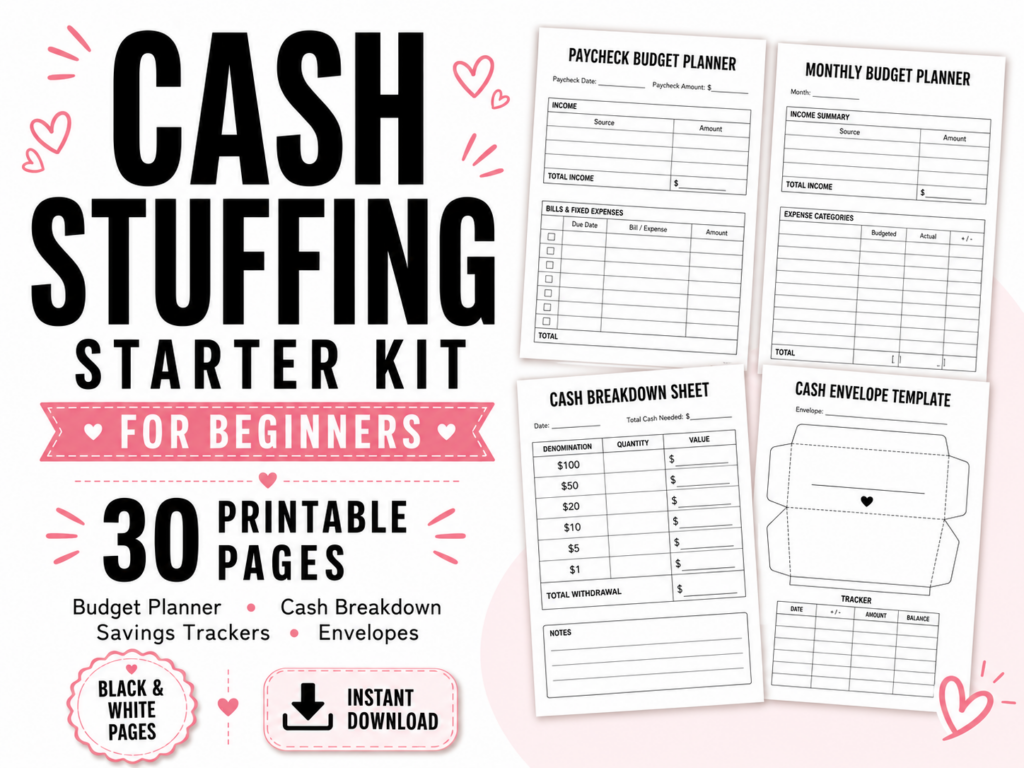

Printable Cash Stuffing Starter Kit for Beginners

If you want an easy way to start, I created a Cash Stuffing Starter Kit for Beginners.

It is a black-and-white, low-ink printable kit designed to help you organize your paycheck and start cash stuffing without feeling overwhelmed.

The kit includes:

- Paycheck Budget Planner

- Monthly Budget Planner

- Bill Tracker

- Cash Breakdown Sheet

- Cash Stuffing Tracker

- Expense Tracker

- Weekly Spending Tracker

- No-Spend Tracker

- Sinking Funds Tracker

- Emergency Fund Tracker

- Christmas Savings Tracker

- Vacation Savings Tracker

- Car Maintenance Tracker

- Debt Payoff Tracker

- Credit Card Payoff Tracker

- Savings Goal Tracker

- $100 Savings Challenge

- $500 Savings Challenge

- $1,000 Savings Challenge

- Cash Envelope Templates

- Category Labels

- Notes Page

You can print the pages at home and use them every payday.

This is a great option if you want a simple printable system instead of trying to create everything from scratch.

How Often Should You Cash Stuff?

Most people cash stuff every payday.

If you get paid weekly, you can cash stuff once a week.

If you get paid biweekly, you can cash stuff every two weeks.

If your income changes from week to week, you can still use the system. Just plan based on the paycheck you actually received, then adjust your categories each time.

The key is to create a payday routine.

A simple routine could be:

- Check your paycheck amount

- List bills due before the next payday

- Choose cash categories

- Fill out your cash breakdown sheet

- Withdraw cash

- Stuff envelopes

- Track spending

- Review before the next paycheck

Do You Have to Use Cash for Everything?

No, you do not have to use cash for everything.

Many people use a hybrid system.

That means they keep fixed bills digital and only use cash for categories where they tend to overspend.

For example, you may keep these digital:

- Rent

- Utilities

- Phone

- Insurance

- Subscriptions

- Debt payments

And use cash for these:

- Groceries

- Gas

- Eating out

- Fun money

- Beauty

- Household

- Kids

This makes cash stuffing easier and more realistic.

Final Thoughts

Cash stuffing is a simple way to organize your paycheck, plan your spending, and stay more aware of your money.

You do not need a perfect budget to start. You just need to choose a few categories, plan your bills first, and give every dollar a job.

Start small. Pick 3 to 5 envelopes. Track your spending. Review what worked. Then adjust on your next payday.

Over time, cash stuffing can help you feel more in control of your money and more prepared for future expenses.

If you want a beginner-friendly printable system, you can check out my Cash Stuffing Starter Kit for Beginners here: